Why I use finpension for my Swiss Pillar 3a and why I think it is one of the best choices for long-term investors

When I moved to Switzerland from Italy, one of the first financial concepts I had to understand was the Swiss Pillar 3a. At the beginning, it looked complicated: tax deductions, pension accounts, insurance products, investment strategies, banks, apps, withdrawal rules.

After using the system for several years, my opinion is now very clear: if you live and work in Switzerland and you want to build long-term wealth efficiently, Pillar 3a is one of the first things you should understand.

And if you are comfortable investing for the long term, I personally think finpension is one of the best Pillar 3a solutions available in Switzerland.

It combines three things I care about a lot:

- Tax savings

- Low fees

- The possibility to invest almost fully in global equities

That combination is powerful.

What is Pillar 3a in Switzerland?

Switzerland’s pension system is built around three pillars.

The first pillar is the state pension system. The second pillar is your occupational pension, usually connected to your employer. The third pillar is your private pension saving.

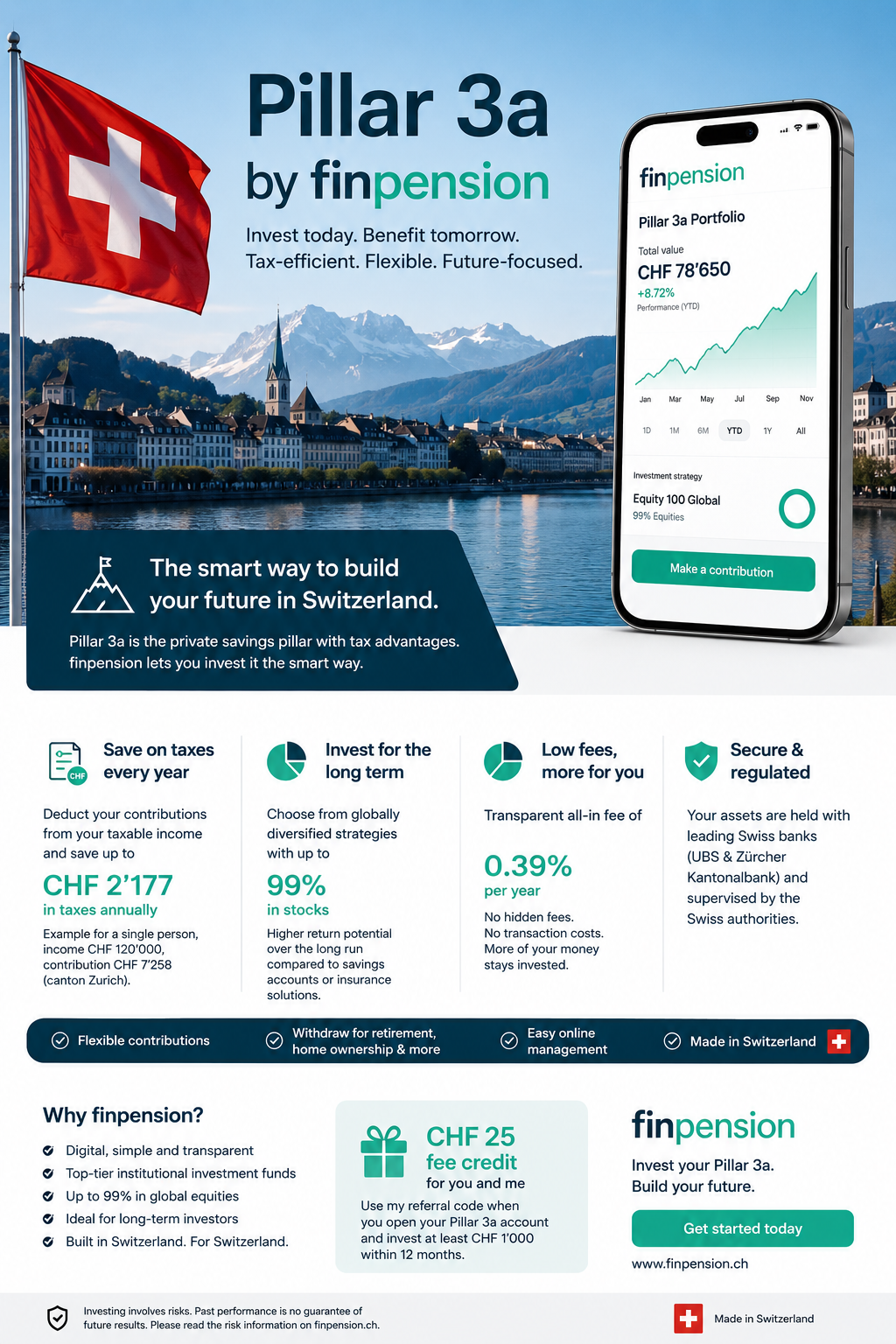

Pillar 3a is the restricted, tax-advantaged part of the third pillar. It is voluntary, but the Swiss government gives you a clear incentive to use it: money paid into Pillar 3a can be deducted from your taxable income, within the legal annual limits. In 2026, employees with a pension fund can contribute up to CHF 7,258, while self-employed people without a pension fund can contribute up to CHF 36,288.

The money is not completely liquid. Pillar 3a is designed for retirement, so withdrawals are restricted. You can usually withdraw it at retirement, or earlier in specific cases such as buying a home, leaving Switzerland permanently, becoming self-employed, or receiving a full disability pension. Withdrawals are taxed separately at a preferential rate, but they are still taxed.

In simple words: Pillar 3a is a tax-efficient retirement account.

How Pillar 3a helps you save tax money

The main immediate advantage of Pillar 3a is the tax deduction.

For example, if you contribute the 2026 employee maximum of CHF 7,258, your taxable income is reduced by CHF 7,258. The exact tax saving depends on your canton, municipality, income, church tax status, marital status, and children.

As a rough estimate, the saving is often somewhere around:

| Marginal tax rate | Approximate tax saving on CHF 7,258 |

|---|---|

| 15% | CHF 1,089 |

| 20% | CHF 1,452 |

| 25% | CHF 1,815 |

| 30% | CHF 2,177 |

This equals to a possible tax saving of up to CHF 1,530 for a single 40-year-old with CHF 120,000 gross income contributing CHF 7,258.

That is why I see Pillar 3a as one of the cleanest financial wins in Switzerland. You are not doing something exotic. You are simply using a legal tax deduction created for retirement saving.

The usual Pillar 3a options: bank or insurance

Most people in Switzerland encounter Pillar 3a through one of two channels:

1. A bank Pillar 3a account

This is the simplest version. You deposit money into a restricted 3a savings account. It is safe and easy to understand. The downside is that the expected return is usually low. For someone close to retirement, this can make sense. For someone with 20, 30, or 40 years ahead, I personally find it too conservative.

2. A Pillar 3a insurance product

Insurance-based 3a products often combine retirement saving with insurance coverage, such as death or disability protection. This can sound attractive, but I am personally not a fan of mixing insurance and investing.

The problem is flexibility. A normal 3a account or investment solution lets you decide how much to contribute each year. With many insurance products, you commit to regular premiums. If your life situation changes, that can become uncomfortable. Independent Swiss finance blogs have also criticized life-insurance 3a products for high costs, lower flexibility, and weak long-term investment outcomes.

My view is simple: buy insurance when you need insurance, and invest when you want to invest. Do not unnecessarily mix the two.

Why investing your Pillar 3a can be much better than leaving it in cash

A 3a savings account gives stability. That is useful if you are close to retirement or if market fluctuations make you nervous.

But if your time horizon is long, I believe investing is much more attractive.

The reason is compounding.

Let’s take a simplified example. Imagine contributing CHF 7,258 per year for 30 years.

| Scenario | Assumed annual return | Approximate value after 30 years |

|---|---|---|

| Cash-like 3a | 0.5% | CHF 234,000 |

| Invested 3a | 4.0% | CHF 407,000 |

| Invested 3a | 5.0% | CHF 482,000 |

These are not guarantees. Markets go up and down, sometimes dramatically. But over long periods, equities have historically been one of the strongest ways to build wealth. finpension itself states that with shares, investors have the chance of significantly higher long-term returns than with a 3a savings account.

For me, this is the key point: Pillar 3a money is usually locked for decades anyway. That makes it a natural place for long-term investing.

If you are 30, 35, or 40 and you will not touch this money for many years, holding everything in cash may feel safe, but it can be very expensive in opportunity cost.

What is finpension?

finpension is a Swiss digital provider focused on pension and investment solutions. For Pillar 3a, it offers both a traditional 3a account and an investment solution inside the same app. Their Pillar 3a product was launched in 2020, and the company says the 3a solution has more than 25,000 customers.

What makes finpension stand out is not just that it is digital. The real advantage is the structure of the investment product.

With finpension, you can invest your Pillar 3a using institutional pension funds from providers such as Swisscanto and UBS. These are funds normally used by pension institutions, not typical retail ETFs. finpension explains that these pension funds can have advantages such as reduced withholding tax on foreign dividends.

The custody banks listed for the finpension 3a foundation are UBS and Zürcher Kantonalbank, and the foundation is supervised by the BVG/LPP and Foundation Supervisory Authority for Central Switzerland.

That gives me comfort. It is modern and app-based, but it is not some random offshore investing app. It is a Swiss pension product with a proper foundation structure.

How finpension Pillar 3a works

The process is simple.

You open a finpension 3a portfolio, choose an investment strategy, deposit money or transfer an existing 3a account, and your deposits are automatically invested according to your selected strategy. Deposits are invested in the selected strategy on the second bank working day of the week.

You can choose from different strategies with different equity allocations, including the high-equity finpension Equity 100 strategy. finpension offers strategies in Global, Swiss, and Sustainable versions, and the strategies can also be customized.

This is where finpension becomes extremely attractive for long-term investors: you can invest almost fully in equities. The highest-equity setup is at around 99% invested in stocks, and finpension’s own strategy name is Equity 100.

For someone like me, this is exactly what I want from a Pillar 3a provider: a low-cost, high-equity, long-term investment solution.

The fees: why 0.39% matters a lot

Fees matter. They matter much more than people think.

finpension’s flat management fee is 0.39% per year. The official fee schedule lists a flat-rate administrative fee of 0.39% p.a., with custody and implementation fees, transaction costs, and strategy changes shown as free of charge.

On the investment page, finpension also states that the investment strategies are implemented with fee-free funds, meaning no additional fund TER for those strategies, and that no transaction or custody fees are charged.

This is a big deal.

A difference of 1% per year may sound small. It is not. Over decades, 1% less in fees can mean tens of thousands of francs more for you. finpension itself states that its pension funds are about 1% cheaper than comparable offers from established banks, mainly due to lower investment costs and withholding-tax advantages.

This is one of the main reasons I like finpension so much: more of your money stays invested for you.

Why I personally recommend finpension

I moved to Switzerland from Italy around four years ago, and since then I have been using finpension for my own Pillar 3a.

I do not recommend it because it is trendy. I recommend it because the product makes sense.

For me, the ideal Pillar 3a provider should be:

- Low-cost

- Transparent

- Flexible

- Easy to use

- Focused on long-term investing

- Able to invest globally

- Not tied to an expensive insurance contract

finpension checks all these boxes.

I especially like that I can choose a very high equity allocation. Since my Pillar 3a money is long-term retirement money, I do not want it sitting in cash for decades. I want it invested in productive assets.

Of course, this is not risk-free. If you invest in stocks, your portfolio will go down during market crashes. A high-equity Pillar 3a is not for someone who panics when markets fall. But for long-term investors who understand volatility, I believe this is exactly the kind of product that makes sense.

My personal opinion is very clear: if you live in Switzerland, have a long time horizon, and want a serious Pillar 3a investment solution, finpension should be very high on your list.

My finpension referral code

If you decide to open a finpension Pillar 3a account, you can use my referral code:

9S817K

With this code, both of us receive CHF 25 in fee credit if you register for a Pillar 3a account and pay in or transfer at least CHF 1,000 within 12 months.

Important: this is a fee credit, not cash paid to your bank account. But since finpension charges a management fee, it effectively reduces your cost.

Final thoughts

Pillar 3a is one of the most useful financial tools available to people working in Switzerland.

You can reduce your taxable income, invest for retirement, and build long-term wealth in a tax-efficient way. But the provider you choose matters. A lot.

For me, the worst mistake is to treat Pillar 3a as something boring and leave it in a low-return account for decades. The second mistake is locking yourself into an expensive and inflexible insurance product without fully understanding the costs.

My preferred approach is simple:

Use Pillar 3a every year, keep fees low, invest for the long term, and avoid unnecessary complexity.

That is why I use finpension, and that is why I recommend it.